9/7/2026

Market Insights

Vietnam has been making international headlines as an industrial manufacturing powerhouse, mostly FDI-fueled, export-driven and further accelerated by the US-China trade confrontation.

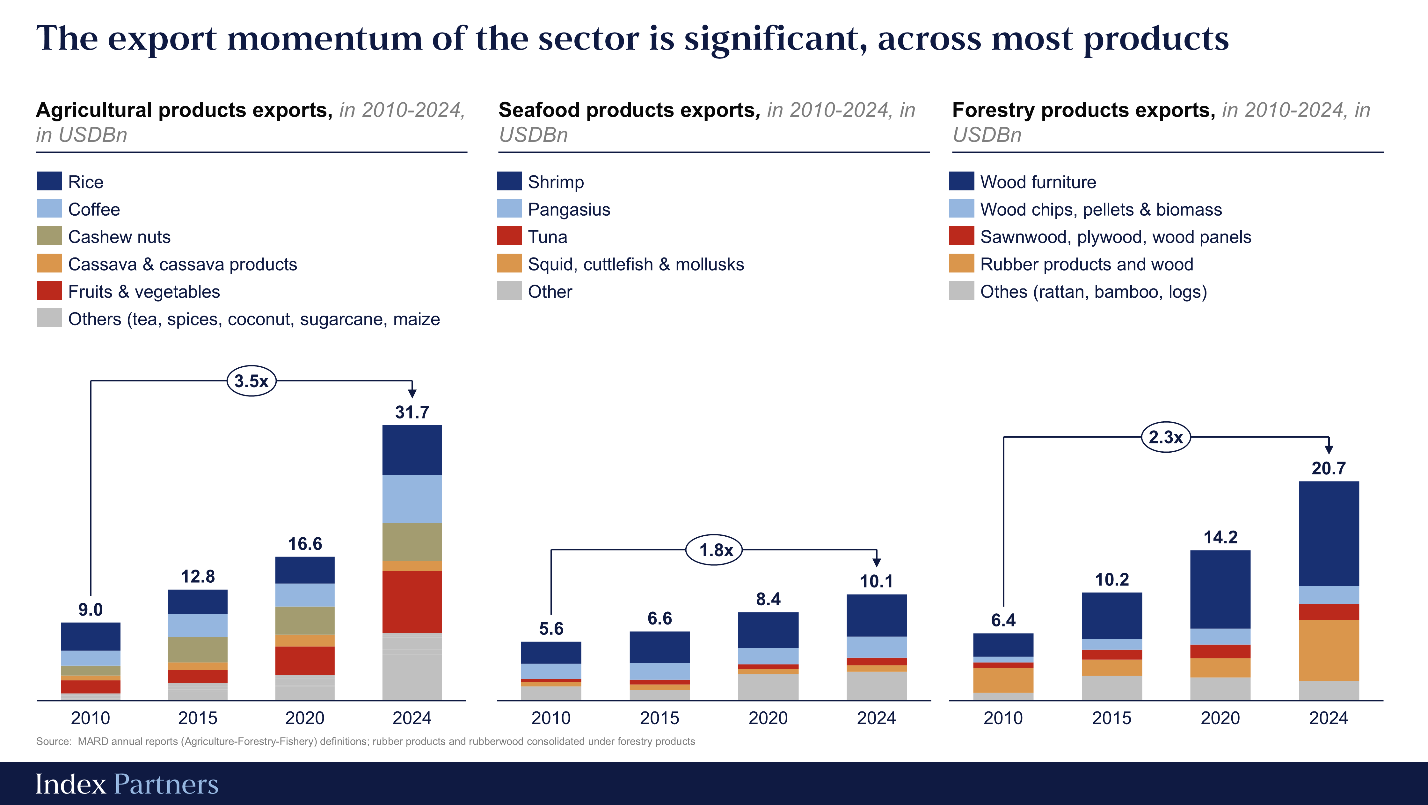

Further from the spotlight, a quieter revolution has been unfolding in a sector built not by foreign capital, but from within: Agriculture. As industrialization accelerated, the agri-food sector held its share of the economy and, more consequentially, turned outward. Agricultural exports reached USD62.5bn in 2024 up nearly 19% in a single year, nearly four times their level fifteen years earlier (Exhibit 4).

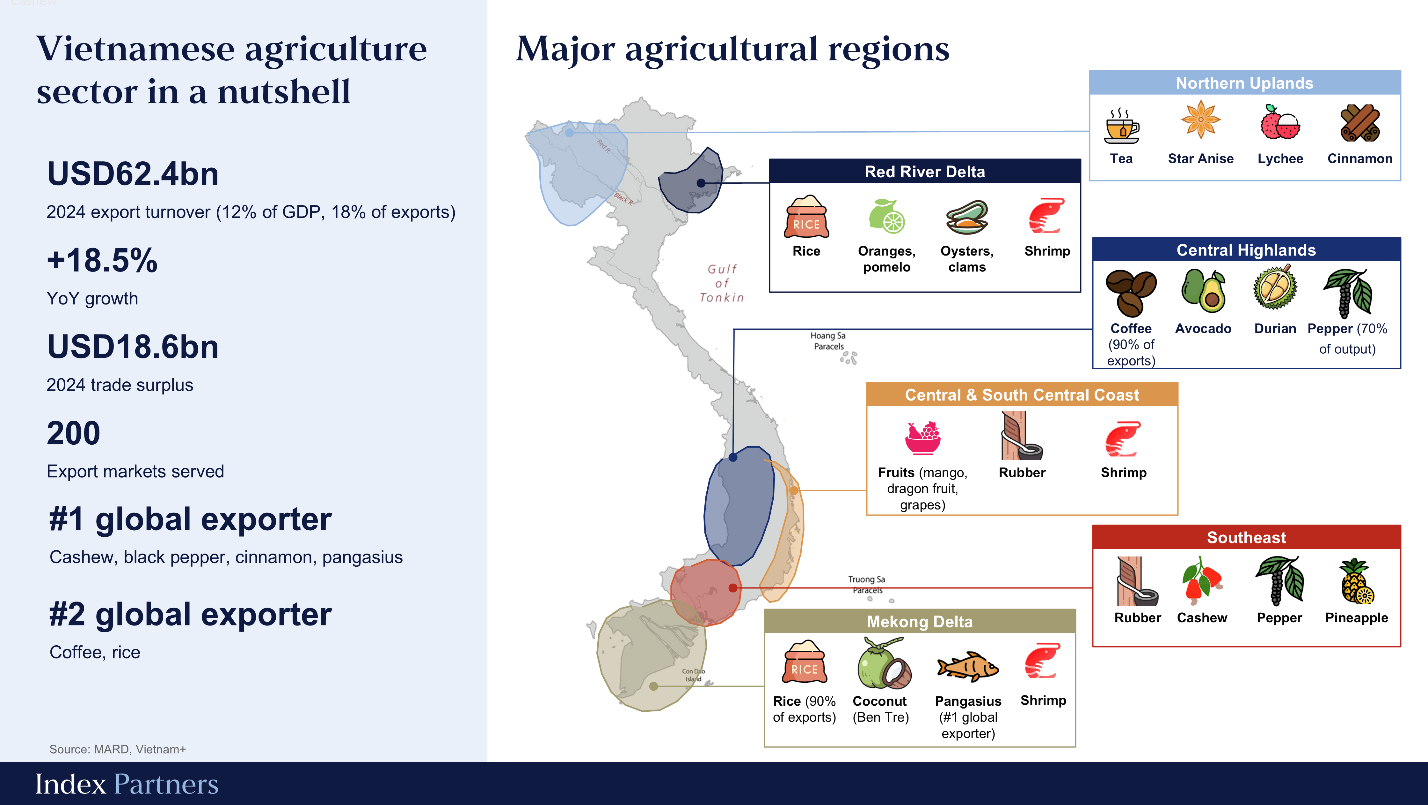

Agriculture employs roughly a third of Vietnam's workforce and contributes close to 12% of GDP, figures that would be unremarkable in isolation. What sets Vietnam apart is how much of that production flows outward: Vietnam is the world's largest exporter of cashew nuts, robusta coffee, pepper, cinnamon, and pangasius fish; the second largest exporter of rice, and the third largest in seafood. These are dominant positions in global commodity markets, built over decades of focused investment in specific value chains by farmers, traders and processors.

What makes Vietnamese agriculture successful is a combination of geography, climate, and accumulated agricultural knowledge that is difficult to replicate. Stretching over 1,600 kilometers from north to south, Vietnam crosses multiple climate zones. Tea and cinnamon thrive in the northern highlands, coffee and pepper in the central plateau, fruit and rice in the south, and aquaculture runs the full length of the coast and along waterways. The Central Highlands sit on a belt of fertile basalt soil at altitude, producing conditions that are nearly ideal for robusta coffee. Vietnam's coffee yields per hectare are among the highest in the world. (Exhibit 1)

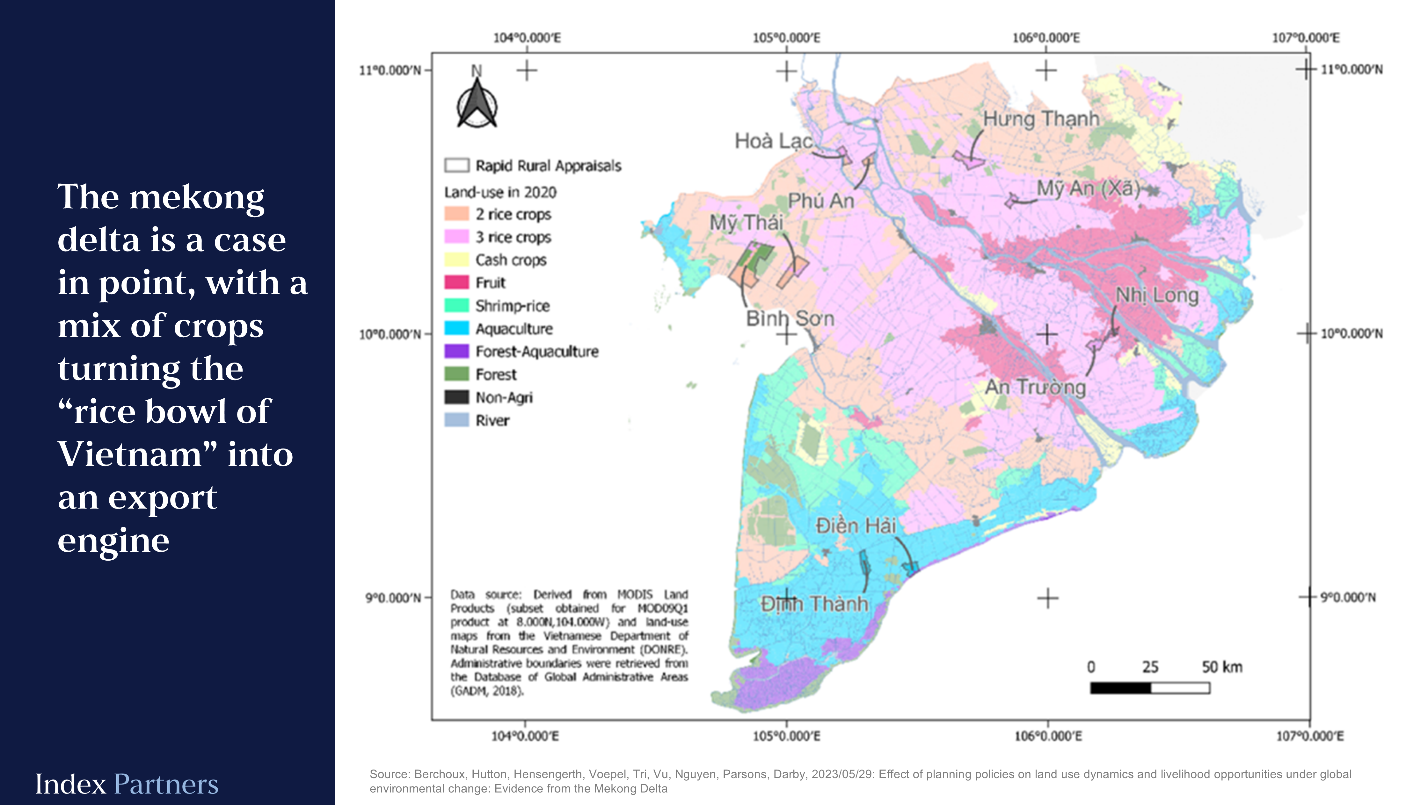

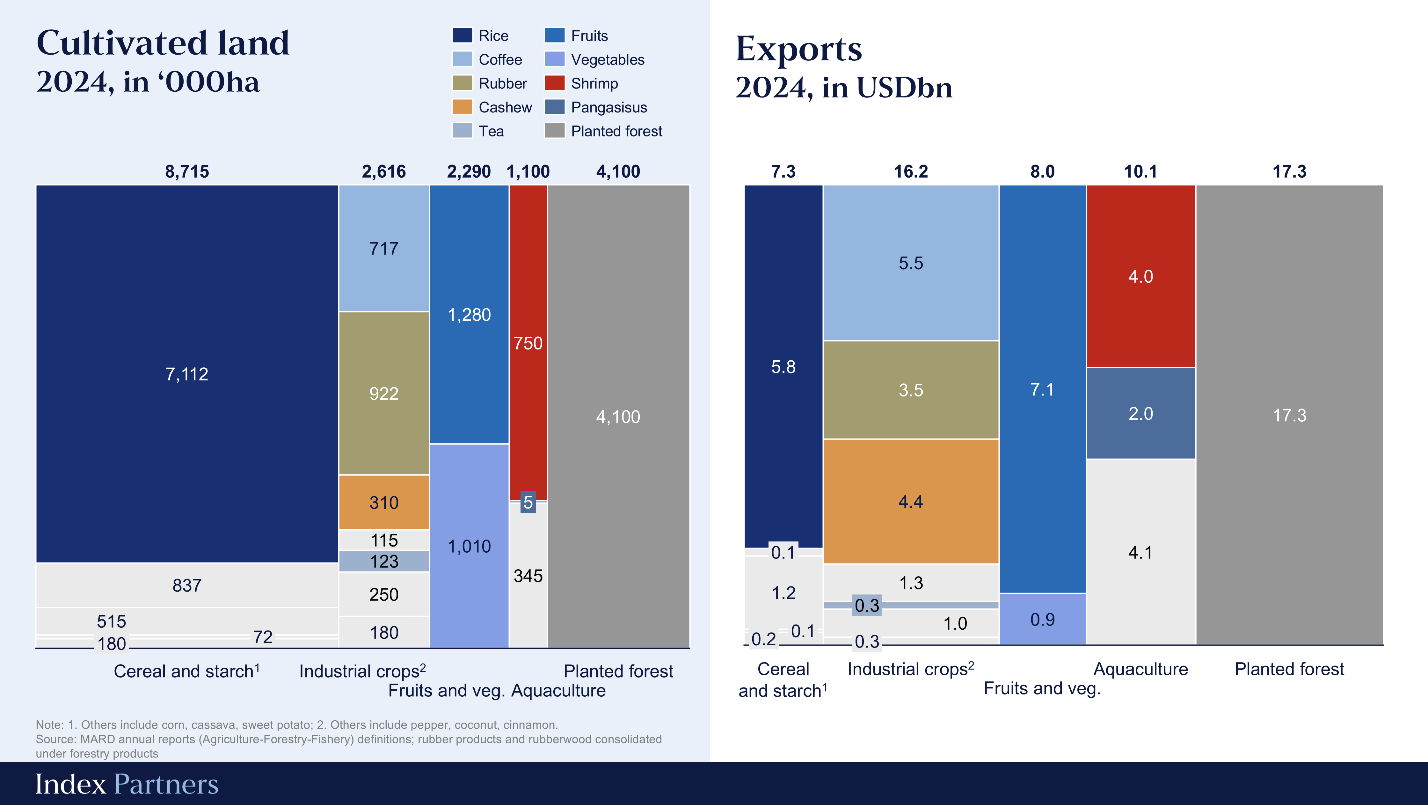

But if there is one place that captures the productive intensity of Vietnamese agriculture, it is the Mekong Delta. An area roughly the size of the Netherlands generates 90% of Vietnam's rice exports, 70% of its fruit production, and 60% of its seafood. The delta is fed by a river system that deposits nutrients across millions of hectares of flat, canal-laced farmland. The growing season never really ends. Rice farmers here take two crops a year as a matter of routine and a third where water management allows. In the drier coastal zones, farmers have developed an ingenious rotation system: flood the paddies with saltwater in the dry season to raise shrimp, flush them fresh in the wet season to grow rice. (Exhibit 2)

The delta is also where Vietnam's durian story began. From near-zero exports in 2020, Vietnam shipped USD4bn worth of durian in 2025, almost entirely to China, after Beijing approved direct fresh imports in 2022. Dak Lak and Tien Giang provinces scaled within two years in a way that would have seemed implausible before. Even if recent concerns got media attention in 2025-2026 (notably related to cadmium contamination and depleted prices with fierce regional competition), the momentum seems to continue with a target of USD4bn in export value for 2026, and a planned market entry into India scheduled in June.

The national ambition is significant, as Vietnam is targeting USD100bn in agricultural, forestry, and fisheries exports by 2030, roughly 60% above where the sector stands today. Reaching that target will require more than business-as-usual productivity gains. The sector is navigating three simultaneous transitions, each of which demands structural adaptation.

The first is climate change. The Mekong Delta is one of the most climate-vulnerable landscapes on the planet. Sea levels are rising, groundwater and sand extraction are causing land subsidence, upstream damming has reduced the sediment flows necessary to replenish the delta's fertility and ultimately saline intrusion is pushing further inland each dry season. The World Bank estimates that without sustained investment in adaptation infrastructure (drainage, flood barriers, salinity-resistant crop varieties, precision irrigation) the delta could see millions of inhabitants displaced and a significant share of its agricultural output impacted by mid-century.

The second transition is around quality and international standards. Exporting to Europe, Japan, and the United States requires compliance with increasingly demanding food safety protocols, pesticide residue limits, and traceability requirements. The debate around EUDR or US import regulations tends to attract the headlines, but the more fundamental challenge is linked to the fact that Vietnam's upstream production remains fragmented in some sectors. Rice, pepper, and coffee are largely grown by smallholders who often lack access to technical support and certification programs. The real challenge is not just adapting to a new regulation, but it's aggregating consistent, traceable, and safety-compliant output from hundreds of thousands of small-scale producers.

The third transition is the changing shape of domestic demand. As Vietnam's middle class expands, preferences are rapidly shifting toward quality and safety, i.e., 74% of Vietnamese consumers cite food safety as an important concern, surpassing the Asia Pacific average of 68%. Consumers increasingly ask where food comes from, how it was grown, and whether the supply chain can be trusted. This creates opportunity for producers: those who invest in provenance and quality documentation can capture premium domestic pricing.

These three pressures are not impacting all sub-sectors equally, and the agricultural landscape is fragmenting along a new line: between sectors that are consolidating and modernizing, and those that are struggling to do so.

Some value chains have made real progress. The swine industry, for example, has undergone consolidation over the past decade. Large integrated operators have displaced significant volumes of smallholder production, bringing biosecurity standards, feed efficiency, and supply chain traceability that smallholders cannot easily replicate. The same dynamic is visible across other areas such as the feed mill sector, farmed shrimp at the processing end, and some specific fruit export chains (coconut, banana, etc.).

Others remain fragmented in ways that are beginning to affect competitiveness. Rice, despite its symbolic importance and export volume, is cultivated by millions of households on plots averaging well under a hectare. Coordination across a base of that size is difficult, and even long-standing, large-scale players sometimes struggle to make contract framing work. Consequently, the export sector still competes largely on price rather than quality premiums, making it slow to adopt the practices that premium markets require. Shrimp farming faces similar structural constraints. Even as processing has become more sophisticated, the farming level is held back by two main issues: deep fragmentation and poor water quality leading to diseases, causing harvest success rates to fall way below 50%. Faced with these odds, a growing number of farmers are quietly walking away from shrimp farming. Sugarcane also illustrates the challenge well: milling capacity remains underutilized; cost competitiveness lags regional peers, and reaching scale will require continued investments from industrials and government support.

The gap between consolidated and fragmented value chains seems to be widening. Sectors where scale, standards, and integration have sufficiently advanced are increasingly attracting capital and growing export value; sectors where fragmentation persists are finding that raw volume is not sufficient to protect market share anymore.

What is drawing international investor attention is a shift in the nature of the companies operating in this sector. Some feed mills have reached industrial scale. Several aquaculture operators have built integrated operations from hatchery to cold storage. Coffee processors are investing in traceability systems and premium certifications. Coconut processing companies in Ben Tre export to more than 90 countries with consistent food safety compliance. These businesses now have the systems, scale, and governance that institutional investors can engage with.

The investment narrative has also been reinforced by a series of crop stories that have caught global attention. The durian super-cycle is the most prominent example, but the momentum is broad-based. Pepper, for instance, is experiencing a price recovery after years of weakness, with 2025 export values jumping nearly 26%. Cashew producers are capturing global health food trends by shifting toward value-added processing, unlocking premium market margins. Coffee exports have reached record highs, fueled not just by tight global supply but also by premium markets seeking out certified and traceable origins. Pangasius, which Vietnam has dominated for two decades, is being re-rated as buyers increasingly value the supply chain reliability that Vietnamese producers offer. Each of these stories tells investors something slightly different, but the common thread is a sector generating returns at scale.

Investment from larger firms - both domestic and international - brings something Vietnam's agricultural sector genuinely needs. Capital is the obvious contribution, though market access, technical standards, and supply chain discipline matter at least as much. When a European animal feed company acquires a Vietnamese feed mill, it brings formulation technology, biosecurity protocols, and direct links to global quality requirements that domestic producers would take years to develop independently. When a Japanese trading company builds a joint venture around Vietnamese beef, it simultaneously creates a market for Vietnamese product in Japan and raises the production standard domestically.

Foreign capital flowing into processing, cold chain, and input services rather than directly into land ownership can help bridge the consolidation gap, sidestepping the land tenure complications that direct consolidation creates. International investors with experience in climate-smart agriculture, precision irrigation, and flood-resistant crop varieties can accelerate the adaptation that the Mekong Delta needs in ways that domestic sources alone cannot easily supply.

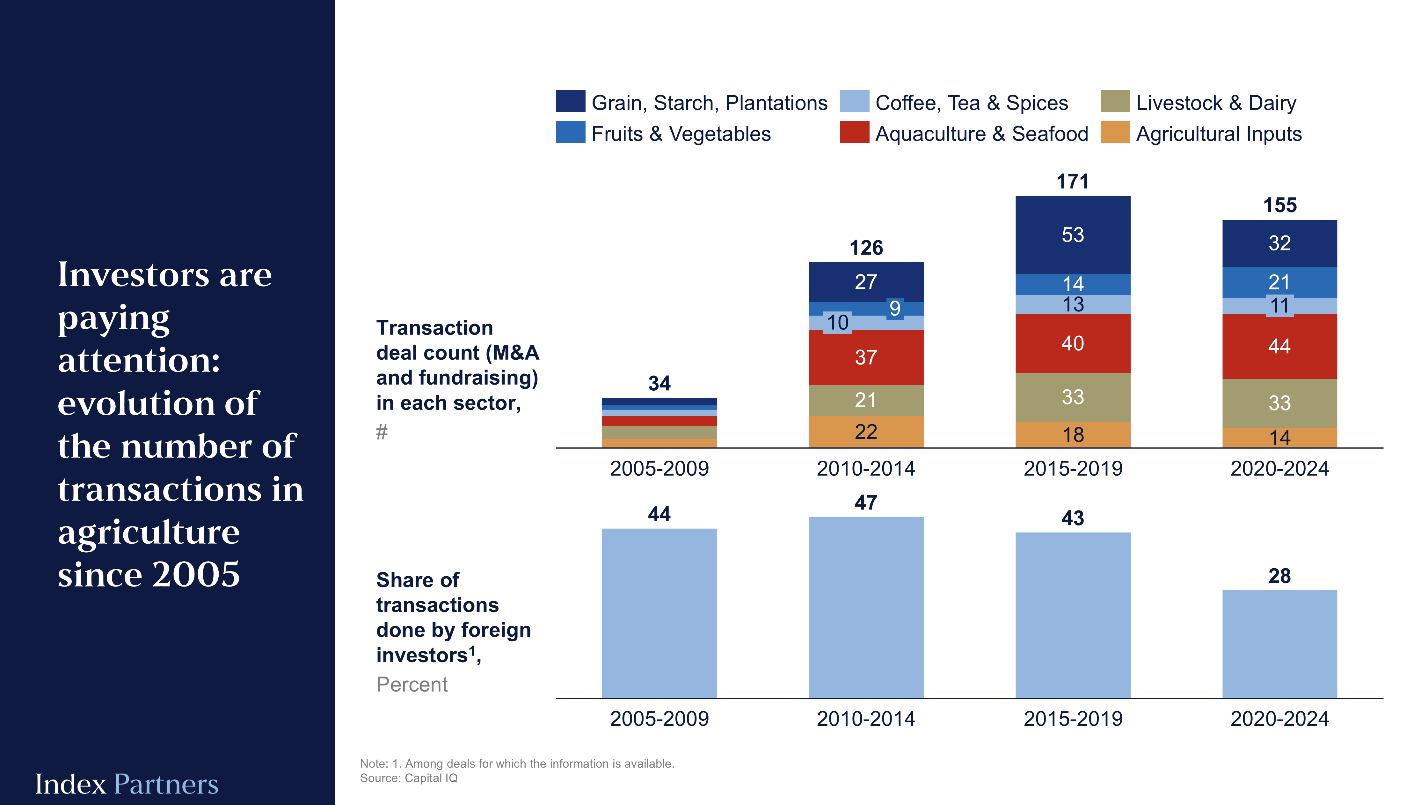

We have seen this shift materialize in the data (Exhibit 5). While only 34 transactions in the sector had been identified between 2005 and 2009, this number scaled to 126 in 2010-2014, and 171 in the years 2015-2019. More recent data points to a stabilization of the deal flow whit a greater share of deals now led by domestic investors: this could point to the maturity of the sector, with more stakeholders able to consolidate through M&A.

At Index Partners, we have had a close view of this sector's momentum over the past years: six of our transactions (across fruits, coffee, seafood, sugar, coconut, and rice) confirmed the patterns: more investor-worthy companies, more foreign capital flowing into the sector. Vietnam's industrial transformation was written by FDIs. Its agricultural transformation was mostly written by Vietnamese farmers, processors, and traders and largely without foreign capital. That is changing fast. As agricultural companies are finding their moment, Index Partners will be here to help Vietnamese companies make the most of it.